Saving Money

Let me be honest with you — I used to be terrible with money.

Not “oh I splurge on coffee sometimes” terrible. I mean genuinely, painfully bad. At 27, I had a decent job, no massive debts, and somehow, by the 22nd of every month, I was staring at my bank app wondering where everything went. Sound familiar?

That was five years ago. Today, I have an emergency fund that could cover six months of expenses, a small investment portfolio, and — here’s the part that surprised even me — I don’t feel like I’m living a restricted life. I still eat out. I still travel. I just stopped bleeding money in places that didn’t actually make me happy.

This guide isn’t about cutting coupons or giving up everything you enjoy. It’s about building a system that works while you sleep, makes decisions easier, and slowly turns you into someone who has money instead of someone who spends money.

Why Most Saving Advice Fails (And What Actually Works)

You’ve probably read the usual tips. “Skip your morning latte.” “Pack your lunch.” “Cancel Netflix.”

Here’s why that advice rarely sticks: it focuses on deprivation rather than design. Willpower is a terrible long-term strategy. It’s like holding your breath underwater — you can do it for a bit, but eventually, you’re gasping.

What actually changed my financial life wasn’t discipline. It was automation and awareness. Once I set up the right systems, saving became something that happened to me, not something I had to force myself to do every single day.

Let me walk you through exactly how I did it — and how you can too.

Step 1: Figure Out Where Your Money Actually Goes

Before you save a single rupee or dollar, you need to know where your cash disappears. I thought I knew. I was wrong by a laughable margin.

Here’s what I did:

- Downloaded my last three months of bank statements. Most banking apps let you export these as PDFs or CSV files.

- Sorted every transaction into categories. Food, transport, subscriptions, shopping, bills, random ATM withdrawals I couldn’t even remember.

- Used a tracking app to keep going. I personally started with Monefy because it’s dead simple — you just tap a category and enter the amount. Some people prefer YNAB (You Need A Budget), which is more powerful but has a learning curve. Wallet by BudgetBakers is another solid option.

The result shocked me. I was spending nearly 18% of my income on food delivery apps alone. Not groceries. Not nice restaurant dinners. Just random Tuesday night orders because I was too lazy to cook.

Your action step: Spend one evening going through your last 90 days of transactions. Don’t judge yourself. Just observe. Write down the three categories where you spent more than you expected. Those are your gold mines for saving.

Step 2: Pay Yourself First (No, Really — Automate It)

This single habit did more for my finances than everything else combined.

The day after my salary hits my account, a fixed percentage automatically transfers to a separate savings account. I started with just 10%. It felt invisible. After three months, I bumped it to 15%. Today, it’s at 25%, and honestly, I barely notice because I never see that money in my spending account.

How to set this up:

- Open a separate savings or deposit account. Ideally one that’s slightly inconvenient to access — no linked debit card, no instant transfers. You want a tiny bit of friction between you and that cash.

- Set up a standing instruction or auto-transfer with your bank. Schedule it for the day after payday.

- Treat this transfer like a bill. Rent is non-negotiable. Electricity is non-negotiable. Your savings transfer? Also non-negotiable.

The beauty of this approach is that you’re budgeting with what’s left, not trying to save what’s left after budgeting. That’s a small distinction that changes everything.

Step 3: The 48-Hour Rule for Non-Essential Purchases

I picked this trick up from a coworker, and it’s saved me thousands.

Whenever I want to buy something that isn’t a basic necessity — a gadget, new shoes, a piece of furniture, some random kitchen appliance I saw on Instagram — I wait 48 hours before purchasing.

That’s it. No complex formula. Just wait two days.

You’d be amazed how often the urge fades. That air fryer I was convinced I needed? Forgot about it in a day. The noise-cancelling headphones? Still wanted them after 48 hours, so I bought them guilt-free.

This rule doesn’t stop you from buying things. It stops you from buying things impulsively. There’s a massive difference. Impulse purchases are where a frightening chunk of money vanishes — studies suggest they account for nearly 40% of all e-commerce spending.

Pro tip: When the urge hits, add the item to your cart but don’t check out. Or add it to a wishlist. Most of the dopamine rush comes from the act of choosing, not the actual purchase. You’ll get the little thrill without the bank statement regret.

Step 4: Attack Your Subscriptions Like Weeds in a Garden

Subscriptions are sneaky. Each one feels small — a few hundred here, a couple of dollars there. But they add up like weeds. You ignore them for a season, and suddenly your entire garden is overrun.

I sat down one evening and listed every recurring charge on my accounts. The total was embarrassing. I had:

- Two music streaming services (one I’d forgotten about entirely)

- A cloud storage plan I wasn’t using

- A gym membership I hadn’t used in four months

- Three different streaming platforms

- An app subscription from a “free trial” I never cancelled

I cancelled five subscriptions that evening. Monthly savings? Roughly the equivalent of a nice dinner for two. Every single month. Forever.

Tools that help: Apps like Trim or Truebill (now called Rocket Money) scan your accounts and flag recurring charges. If you’re not comfortable with third-party apps accessing your bank data, a manual audit works just as well — it just takes an hour of your time.

Related reading: How to Audit Your Monthly Subscriptions and Stop Wasting Money

Step 5: Build an Emergency Fund Before You Do Anything Fancy

I know investing sounds exciting. Crypto, stocks, mutual funds — everyone’s talking about it. But here’s the uncomfortable truth: if you don’t have an emergency fund, you’re building a house on sand.

When my car broke down two years ago, the repair bill was steep. If that had happened during my broke-at-27 phase, I would have put it on a credit card and spent months paying interest. Instead, I pulled it from my emergency fund, topped it back up over the next couple of months, and moved on. No stress. No debt spiral.

How much should you save?

The textbook answer is three to six months of essential expenses. But don’t let that number paralyze you. Start with a target of one month’s worth of rent and bills. That single month of buffer will make you sleep better than you have in years.

Keep this fund somewhere accessible but not too accessible. A high-yield savings account works perfectly. You want it liquid enough for real emergencies but not so convenient that you dip into it for a weekend getaway.

Step 6: Cook More. Seriously. This One’s Not Optional.

I resisted this advice for years. “I’m too busy.” “I’m a terrible cook.” “It’s just not worth the effort for one person.”

All excuses. Every single one.

When I finally committed to cooking most of my meals at home, my food spending dropped by nearly 40% in the first month. And I’m not talking about elaborate recipes or meal prepping seventeen containers on Sunday afternoon. I’m talking about simple, repeatable meals.

Here’s my lazy rotation:

- Eggs and toast for breakfast (takes four minutes)

- Rice, lentils, and whatever vegetable is cheap for lunch

- Pasta with a quick sauce or stir-fried noodles for dinner

I batch-cook rice and lentils twice a week. Total active cooking time per day? Maybe 25 minutes. The savings compared to ordering food are staggering.

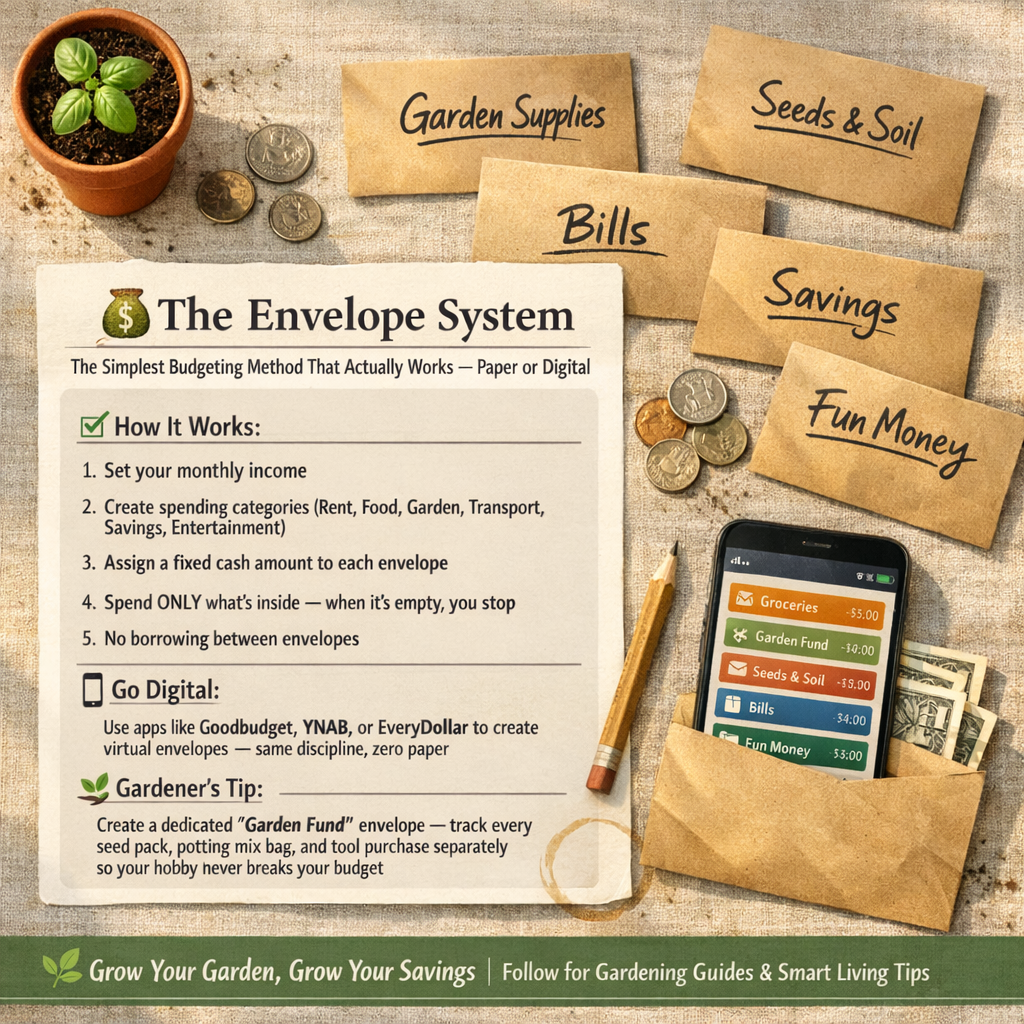

Step 7: Use the Envelope System (Even a Digital Version)

Old-school? Absolutely. Effective? Unbelievably so.

The concept is straightforward: divide your monthly spending money into categories, assign each category a fixed amount, and once that amount is gone, it’s gone.

You can do this with actual cash envelopes if you’re old-fashioned (my grandmother swears by it), or use a digital version. Apps like Goodbudget are designed specifically around this method. Even a simple spreadsheet works — I used Google Sheets for months before switching to an app.

The psychological shift is powerful. Instead of thinking “Can I afford this?” you think “Is this worth taking from my grocery envelope?” It transforms vague anxiety into concrete choices.

Mistakes I Made That Cost Me Real Money

Let me save you some pain by sharing my worst blunders:

1. Saving in the same account I spend from. This is like keeping chocolate on your desk while dieting. Separate accounts, always.

2. Setting unrealistic saving goals. I once tried to save 50% of my income overnight. Lasted eleven days. Start small. Build momentum. Increase gradually.

3. Ignoring small leaks. I dismissed small daily expenses as “just a few bucks.” Over a year, those few bucks added up to a vacation I could’ve taken.

4. Not tracking after the first month. Tracking your spending for one month gives you a snapshot. Tracking for six months gives you a pattern. The pattern is where the real insights hide.

5. Comparing my progress to others. Personal finance is personal. Someone saving 30% of their income might earn three times what you do, or live in a city where rent is half of yours. Run your own race.

The Mindset Shift That Ties Everything Together

Here’s something nobody told me when I started: saving money isn’t about saying no to things. It’s about saying yes to different things.

Every time I transfer money to savings, I’m not depriving present-me. I’m giving future-me options. The option to quit a job I hate. The option to handle a crisis without panic. The option to say “yes” to an opportunity that requires capital.

That mental reframe turned saving from a chore into something that genuinely feels good. Like watering a plant and watching it grow, slowly, steadily, until one day you look up and realize you’ve built something real.

Quick-Reference Toolkit

Here’s a summary of tools and apps mentioned throughout this guide, plus a few extras worth checking out:

| Tool | Best For | Cost |

|---|---|---|

| Monefy | Simple daily expense tracking | Free / Premium |

| YNAB | Zero-based budgeting | Paid (free trial) |

| Goodbudget | Envelope budgeting | Free / Paid |

| Rocket Money | Subscription management | Free / Premium |

| Google Sheets | Custom budget tracking | Free |

| Wallet by BudgetBakers | All-in-one finance tracking | Free / Paid |

Where to Go From Here

If you’ve read this far, you already have more financial awareness than most people ever develop. But reading and doing are two very different animals.

My challenge to you: pick one step from this guide and implement it this week. Not all seven. Just one. Get that win under your belt, feel the momentum, and then add another.

The path from financially stressed to financially stable isn’t a sprint. It’s a series of small, boring, consistent decisions that compound over time — much like the interest in that savings account you’re about to open.

Five years from now, you’ll look back at this moment the same way I look back at my broke-at-27 self: with a mix of compassion and gratitude. Compassion for how hard it felt. Gratitude for finally starting.

You’ve got this.