52-Week Money Saving Challenge

52-Week Money Saving Challenge: Save $1,378 This Year

Table of Contents

- What the 52-Week Challenge Actually Is

- The Week-by-Week Breakdown

- The Mistake I Made the First Time

- The Reverse Challenge: A Smarter Option for Many People

- Where to Keep the Money

- How to Handle Tough Weeks

- Tracking Without Losing Your Mind

- What Can $1,378 Actually Do?

- Final Thoughts: Why the Challenge Works

Let me be honest with you. The first time I heard about the 52-week money saving challenge, I rolled my eyes a little. “Save a dollar in week one, two dollars in week two… yeah, sure.” It sounded like something posted on Pinterest between a smoothie recipe and a DIY wreath tutorial.

Then I actually tried it. And at the end of the year, I had $1,378 sitting in a savings account I had basically ignored for twelve months. That money paid for a weekend trip to Nashville and covered two months of my car insurance. Not life-changing, but genuinely useful. More importantly, it changed how I thought about saving money — not as a big sacrifice, but as a slow, quiet habit.

If you have ever started a savings goal and abandoned it by February, this challenge is worth a second look. Here is everything I wish someone had told me before I began. Read our Saving Money guide.

What the 52-Week Challenge Actually Is

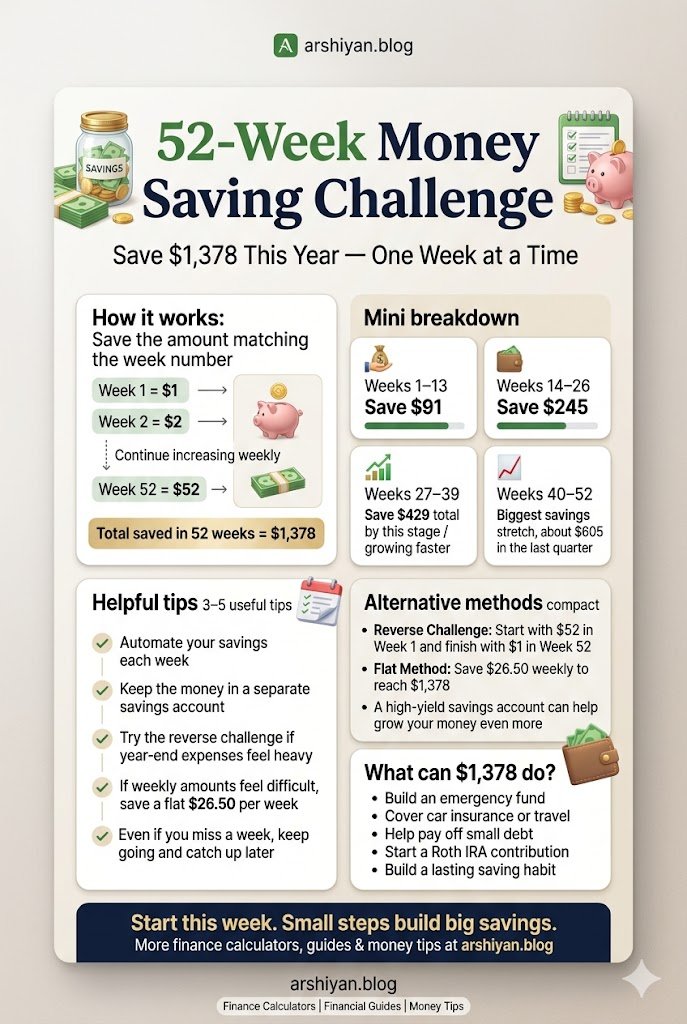

The concept is beautifully simple. Every week of the year, you save an amount equal to the week number. Week 1, you save $1. Week 2, you save $2. By Week 52, you save $52.

Add all of that up and the total comes to exactly $1,378.

The beauty is in the structure. You are not saving the same flat amount every week. You start small, which means January barely puts a dent in your wallet. The heavy lifting happens in November and December, when — yes — the amounts get steeper. Week 48 is $48. Week 50 is $50. Weeks 51 and 52 are $51 and $52.

That back-loaded schedule is both a feature and a flaw, and we will get into that.

50 Practical Ways to Cut Monthly Expenses Without Feeling Deprived

The Week-by-Week Breakdown (No Spreadsheet Required)

You do not need to memorize anything fancy. Just save whatever week number it is. But here is a rough quarterly snapshot so you know what to expect:

January through March (Weeks 1 to 13): You save a combined total of $91. This is the “easy” phase. Honestly, you barely notice it. Week 7 is just $7.

April through June (Weeks 14 to 26): The total for this quarter is around $245. You are past the halfway point of the year but still well under $400 saved.

July through September (Weeks 27 to 39): Things start picking up. This quarter adds roughly $357 to your balance. Your savings account should be growing noticeably now.

October through December (Weeks 40 to 52): This is where the challenge gets real. You save around $605 in just thirteen weeks. Week 45 alone is $45. The last three weeks of the year total $153 by themselves.

If you look at those numbers and feel a little nervous about the holiday season overlap, you are not wrong to feel that way. More on that fix in a moment.

The Mistake I Made the First Time

My first attempt at this challenge failed around Week 34. Not because I ran out of money, but because I lost track. I was moving the money manually into a separate account every Friday, and somewhere around August, I skipped a week. Then I forgot which week I was on. Then I just kind of stopped.

This is the most common reason people quit, and it is a totally avoidable problem.

What fixed it for me the second time was automation. I use Ally Bank for my savings account because it lets you set up recurring transfers on a schedule. The problem is, the weekly amounts change, so you cannot just set one recurring transfer.

Here is the workaround that actually worked for me: I used a free app called Qapital (it is available on both iPhone and Android). Qapital has a built-in 52-week challenge rule. You set it up once, connect your checking account, and it automatically moves the right amount every week without you touching anything. You get a notification when it happens, and you can watch your progress on a little visual tracker.

If you prefer to keep it manual, the YNAB (You Need A Budget) app makes it easy to assign the weekly savings as a budget category. You can also just use a plain Notes app on your phone with a running checklist — not glamorous, but it works.

The key is picking one system and sticking to it, not switching tools halfway through.

The Reverse Challenge: A Smarter Option for Many People

The traditional version of this challenge is hardest at the worst time of year. The last eight weeks of December and November, when you are buying gifts, traveling, and eating out more, are also the weeks where you owe $45, $47, $49, $51 and $52. That timing can break the whole thing.

The reverse challenge flips the order. You start Week 1 by saving $52, Week 2 by saving $51, and work your way down. By December, your weeks are in the single digits. Week 52 is just $1.

This approach works better for people who get a year-end bonus, receive a tax refund in February, or just find it easier to stay motivated when they can see a large chunk of savings built up early. The end result is the same $1,378, just arranged differently.

There is also a modified flat method: instead of variable amounts, you save $26.50 every week. That also adds up to $1,378. Some people find the consistency easier to budget around. There is no wrong version here. The best one is whichever one you actually finish.

Where to Keep the Money

Please do not keep this money in your regular checking account. That is like hiding cookies on the kitchen counter and expecting not to eat them.

The two best options right now for Americans doing this challenge:

High-Yield Savings Accounts (HYSAs): SoFi, Marcus by Goldman Sachs, and Discover all offer competitive rates with no monthly fees. Even at a 4 to 5 percent annual yield (rates vary, always check current offers), your $1,378 will earn somewhere between $30 and $60 in interest over the year. That is a free lunch, essentially.

Credit Union Savings Accounts: If you are a member of a credit union like Navy Federal or a local one in your area, many offer small “holiday savings” or “goal savings” accounts with limited withdrawal access. The friction of not being able to easily pull money out is actually a feature.

Complete Guide to Credit Scores and How to Improve Yours

Avoid putting this money in the stock market for a one-year challenge. The point is that the money is there when the year ends, not riding a market dip in October.

How to Handle Tough Weeks

Life does not pause for your savings challenge. A car repair, a medical bill, a slow pay period — these things happen, and they will happen at some point during 52 weeks.

The worst thing you can do is skip a week and tell yourself you will catch up later. In my experience, catching up rarely happens, and the guilt of being “behind” is what eventually kills the habit.

Instead, try this: if you genuinely cannot hit the full amount for a particular week, save whatever you can. Even $5 in a $38 week is better than $0. Make a note and catch up the difference during a week when you have a little extra, like a week you get a bonus, a side gig payment, or a gift.

Think of it like a long road trip. If you hit traffic for one hour, you do not turn around and go home. You adjust and keep driving.

Tracking Without Losing Your Mind

Here is the simple tracking method that has worked for me without needing any fancy tools:

Step 1: On January 1st, write the numbers 1 through 52 on a piece of paper or in a notes app.

Step 2: Beside each number, write the dollar amount for that week (same as the week number).

Step 3: Every time you make a transfer, check off that week and record the date.

Step 4: At the end of each month, add up your total saved. Compare it to the expected total. This takes five minutes and keeps you honest.

Some people print out a physical tracker and pin it somewhere visible, like a refrigerator or a bathroom mirror. There is genuine psychological value in physically checking off a box. It gives your brain a small hit of satisfaction, which makes you more likely to keep going. This is the same principle behind habit tracking apps like Habitica or even a basic paper habit tracker from a dollar store journal.

What Can $1,378 Actually Do?

Let me make this concrete, because “save $1,378” can sound abstract.

For someone with no emergency fund, this amount covers roughly one to two months of essential expenses depending on your location. That is the difference between a car breakdown being a stressful afternoon versus a financial catastrophe.

For someone already stable, $1,378 could be:

A direct contribution toward a Roth IRA (the 2024 annual limit is $7,000, so this covers about 20 percent of it). A round-trip flight plus hotel for a domestic trip. A head start on a home repair fund. A payoff for a small credit card balance, which depending on your interest rate could save you an additional $150 to $300 in interest. Three to four months of a gym membership, music streaming, and a few nice dinners combined.

The money is not the point by itself. The point is that you built the habit of regular saving, and $1,378 is the evidence of that habit.

Frequently Asked Questions

How to save $5,000 in 52 weeks?

To save $5,000 in 52 weeks, save about $96.15 per week. You can make it easier by automating weekly transfers into a separate savings account.

How much money do you save in the 52-week challenge?

In the standard 52-week money saving challenge, you save $1,378 by the end of the year. You start with $1 in week 1, $2 in week 2, and continue up to $52 in week 52.

How much is $100 a week for 52 weeks?

Saving $100 per week for 52 weeks gives you $5,200. This is a simple flat-rate version of a yearly savings challenge.

What is the $10,000 in 52 weeks challenge?

The $10,000 in 52 weeks challenge means saving about $192.31 per week for one year. Some people use increasing weekly amounts or automatic transfers to stay on track.

How much is $5 a day for 40 years?

Saving $5 a day for 40 years equals $73,000, not including interest. If invested, the final amount could be much higher depending on returns.

One More Thing Worth Saying

A lot of personal finance advice is aimed at people who just need to hear the information. But most of us already know we should save more. The real barrier is follow-through, not knowledge.

The 52-week challenge works not because the math is clever, but because the structure is forgiving. Starting with $1 makes entry so low that there is almost no excuse not to begin. And once you have kept a habit going for eight or ten weeks, the sunk cost of stopping starts to feel worse than the cost of continuing.

Try our free Tools:

Savings Goal Calculator

If you start this challenge in January and make it to March, you are probably going to finish it. That is the dirty secret nobody mentions. Getting started is the whole battle.

So set up the automatic transfer tonight. Use Qapital, use your bank’s app, use a jar on your kitchen counter — whatever matches how your brain works. Just start it this week, even if this week is not Week 1 of the year. Pick up wherever the calendar puts you and go from there.

Twelve months from now, $1,378 will be sitting somewhere waiting for you. That is not a promise from some financial guru on a YouTube channel. That is just arithmetic.

My name is Arshiyan Ahmed, and I write about personal finance because I’ve lived through the stress of financial uncertainty — and found my way out of it.

Over the past 7+ years, I’ve spent hundreds of hours studying budgeting systems, debt payoff strategies, and savings frameworks — not just in theory, but by applying them to real life. I’ve personally used the debt snowball method to eliminate credit card debt, built a 6-month emergency fund on a modest income, and helped friends and family create their first workable budgets.

I started Arshiyan Finance because I noticed one thing: most financial content online is either too complicated for beginners or too generic to be useful. I wanted to build a space where everyday people — whether you’re living paycheck to paycheck or just looking to manage money smarter — could find clear, actionable, and honest financial guidance without being sold something.

Everything I publish here is based on widely accepted financial principles, researched thoroughly, and written in plain language anyone can follow. The calculators, guides, and strategies on this site are the same tools I use and recommend to people I care about.

I’m not a licensed financial advisor, and nothing on this site is professional financial advice — but I do believe that access to good financial education can change lives. That’s why everything here is completely free.

When I’m not writing about money, I’m reading about it — because the more I learn, the better I can explain it to you.

Have a question or topic you’d like me to cover?