Complete Guide to Credit Scores and How to Improve Yours

Complete Guide to Credit Scores and How to Improve Yours

Table of Contents

- What Is a Credit Score, Really?

- How Credit Scores Are Calculated

- The Five Factors That Shape Your Score

- What Your Score Range Actually Means

- Step-by-Step: How to Improve Your Credit Score

- Common Mistakes That Silently Kill Your Score

- Best Tools and Apps to Track and Build Credit

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

There was a time when I applied for a car loan and got rejected without a clear explanation. The dealer handed me a paper with a three-digit number on it — 588 — and said, “Your score needs work.” I didn’t even fully understand what that number meant back then. I just knew it felt like a door slamming in my face.

That frustration sent me down a rabbit hole of credit research that changed how I handle money entirely. Years later, I’ve helped dozens of people understand their credit profiles, dispute errors, and rebuild scores that once felt beyond repair. This guide is everything I wish someone had handed me on that day. Read financial guides

A quick trust note: The information in this article is based on publicly available credit bureau data, FICO scoring methodology, and verified consumer finance research. This is not legal or financial advice — but it is honest, practical, and grounded in real experience.

What Is a Credit Score, Really?

Think of your credit score as a financial report card — except instead of teachers grading your homework, lenders are grading how reliably you pay your debts. The number sits between 300 and 850, and it follows you into almost every major financial decision you make: renting an apartment, buying a car, getting a mortgage, sometimes even landing a job.

The two most common scoring models used in the United States are FICO and VantageScore. FICO is still the gold standard — roughly 90% of top lenders use it when making decisions. VantageScore is used by many free credit monitoring apps and has grown in popularity, but knowing your FICO score is more valuable when you’re preparing for a big purchase.

Here’s the part most people miss: you don’t have just one credit score. You have many. Each of the three major credit bureaus — Equifax, Experian, and TransUnion — holds its own file on you, and your score can differ between them by 20, 30, or even 50 points depending on what each bureau has recorded.

How Credit Scores Are Calculated

FICO doesn’t use magic. The formula is publicly documented, even if the exact algorithm is proprietary. At its core, the model looks at your credit history and tries to predict one thing: how likely are you to miss a payment by 90 days or more in the next 24 months?

Every action you take with credit — opening a card, paying a bill, carrying a balance, closing an old account — gets fed into that calculation.

Try our free tool : debt payoff calculator

The Five Factors That Shape Your Score

1. Payment History — 35%

This is the biggest piece of the pie, and it makes sense. Lenders care most about whether you pay what you owe, when you owe it. One 30-day late payment can drop a good score by 50 to 100 points. A 90-day late is even more damaging, and a collection account can haunt your report for seven years.

What helps: Setting up autopay for at least the minimum payment on every account. You can always pay more manually, but this guarantees you never miss the deadline by accident.

2. Amounts Owed (Credit Utilization) — 30%

This refers to how much of your available credit you’re using. If your credit card limit is $5,000 and your balance is $4,500, your utilization is 90% — and that’s a red flag for lenders. The sweet spot most experts agree on is keeping utilization below 30%, but the people with the highest scores usually keep it under 10%.

A small mental trick: credit utilization is calculated at a single point in time, usually when your statement closes. You can pay your balance down before that date and temporarily look like a much more responsible borrower, even if you use the card heavily throughout the month.

3. Length of Credit History — 15%

Older accounts signal experience with credit. The model looks at the age of your oldest account, your newest account, and the average age across all accounts. This is why closing an old credit card you no longer use can actually hurt you — it shrinks the average age of your accounts.

4. Credit Mix — 10%

Having a mix of revolving credit (like credit cards) and installment loans (like a car loan or student loan) shows that you can manage different types of debt responsibly. You don’t need to go take out a loan just to improve this factor, but it’s worth knowing that variety does matter.

5. New Credit (Hard Inquiries) — 10%

Every time you apply for new credit, the lender pulls a hard inquiry on your report. Each hard inquiry can lower your score by a few points and stays on your report for two years. Applying for five credit cards in two months sends a signal that you may be in financial trouble. Space out applications whenever possible.

What Your Score Range Actually Means

| Score Range | Rating | What It Usually Gets You |

|---|---|---|

| 800 to 850 | Exceptional | Best rates on everything, easy approvals |

| 740 to 799 | Very Good | Excellent rates, rarely denied |

| 670 to 739 | Good | Approved for most products, decent rates |

| 580 to 669 | Fair | Some approvals, higher interest rates |

| 300 to 579 | Poor | Mostly denials or secured products only |

The difference between a 620 and a 760 on a 30-year mortgage could mean paying over $100,000 more in interest across the life of the loan. That three-digit number carries enormous financial weight.

Step-by-Step: How to Improve Your Credit Score

Step 1: Get Your Actual Reports

Go to AnnualCreditReport.com — this is the only federally authorized free source. Pull reports from all three bureaus. Do not use random websites that ask for a credit card upfront. pay off debt to boost your score

Step 2: Read Everything Line by Line

Look for accounts you don’t recognize (possible fraud or identity mix-ups), incorrect late payment dates, balances that don’t match your records, and duplicate entries.

Step 3: Dispute Errors Directly

File disputes online through each bureau’s website:

- Equifax: equifax.com/personal/credit-report-services

- Experian: experian.com/disputes

- TransUnion: transunion.com/credit-disputes

Bureaus have 30 days to investigate. If they can’t verify the item, it must be removed.

Step 4: Tackle Utilization First

This is usually the fastest lever. If you have high balances on revolving accounts, prioritize paying those down before doing almost anything else. Even moving a card balance from 80% utilization to 30% can move your score significantly within one billing cycle.

Step 5: Never Miss Another Payment

Set up autopay immediately on every account. Even one forgotten payment can undo months of progress.

Step 6: Consider a Secured Card or Credit Builder Loan

If your credit history is thin, a secured card or a credit builder loan through an institution like Self (formerly Self Lender) can establish positive payment history without requiring good credit upfront.

Step 7: Ask for a Credit Limit Increase

If you’ve been responsible with an existing card for 6 to 12 months, call the issuer and ask for a higher limit. If they approve it without a hard pull, your utilization drops instantly without you spending a dollar more.

Step 8: Be Patient With the Timeline

Most meaningful improvements take 3 to 6 months to show up. Rebuilding from a poor score to a good one realistically takes 12 to 24 months of consistent behavior. use credit cards to build your score

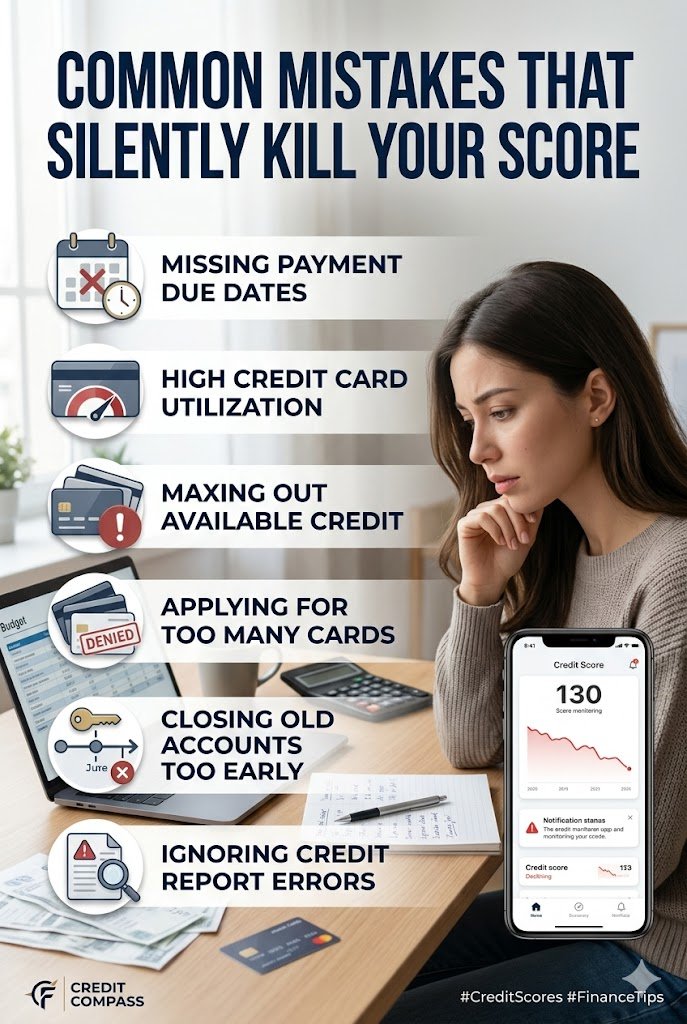

Common Mistakes That Silently Kill Your Score

Closing old accounts you no longer use. It feels responsible, but it reduces your available credit and can shrink your average account age. Unless the card carries an annual fee you can not justify, leave it open and use it for one small purchase every few months.

Applying for multiple cards at once. People do this during holiday shopping or after a big move when they want points and rewards. Each application is a hard inquiry. Space them at least 6 months apart.

Ignoring small collection accounts. A $75 gym membership that went to collections can damage your score just as much as a $3,000 debt. Small balances are easier to negotiate and resolve.

Paying off old collections without checking the date first. If a collection account is five or six years old and nearing the seven-year removal window, paying it could reset the clock in some cases. Always check the original delinquency date before deciding to pay.

Assuming your spouse’s credit doesn’t affect you. It doesn’t — directly. But if you apply for a joint mortgage or loan, both scores are evaluated. A strong score on one end can not always carry a poor score on the other.

financial mistakes that hurt your credit

Best Tools and Apps to Track and Build Credit

Credit Karma — Free, uses VantageScore, updates weekly. Great for monitoring changes and catching unusual activity. Owned by Intuit.

Experian App — Gives you free access to your actual FICO Score 8. The free version is solid. Their Experian Boost feature lets you add utility and streaming payments to your credit file, which sometimes nudges scores upward.

https://www.experian.com/credit/experian-app

Self (self.inc) — A credit builder loan designed specifically for people with no credit or poor credit. You make monthly payments into a savings account, and at the end of the term, you get the money back (minus fees and interest). The payments are reported to all three bureaus.

Discover it Secured Card — One of the best secured cards on the market. No annual fee, earns 2% cash back at gas stations and restaurants, and Discover reviews accounts for upgrade to unsecured status after 7 months of responsible use.

https://www.discover.com/credit-cards/secured-credit-card

myFICO.com — If you want to see your actual FICO scores across all three bureaus and multiple score versions (mortgage lenders use different FICO versions than auto lenders), this is the most detailed paid option available.

Frequently Asked Questions

How long does it take to raise my credit score by 100 points?

It depends on what’s dragging your score down. If the main issue is high utilization, paying down balances can show results in 30 to 60 days. If you have collections or late payments, expect 6 to 12 months of consistent work.

Does checking my own credit score hurt it?

No. Checking your own score is a soft inquiry and has zero impact on your score. Only hard inquiries from lenders affect it.

Can I remove a late payment from my credit report?

You can try sending a goodwill letter to the original creditor asking them to remove it as a one-time courtesy. This works more often than people realize, especially if you have an otherwise clean history with that lender. There is no guarantee, but it costs nothing to ask.

Is 700 a good credit score?

Yes, a 700 puts you in the “good” range and qualifies you for most mainstream financial products. That said, the difference between 700 and 760 is often meaningful in terms of interest rates, especially on mortgages and auto loans.

Will getting married affect my credit score?

Getting married does not merge your credit reports. Your scores stay separate. However, joint accounts and joint loan applications will pull both scores and both histories.

What’s the fastest way to build credit from scratch?

The fastest legitimate path is a combination of becoming an authorized user on someone else’s account with good standing, opening a secured card, and making every payment on time from day one.

Sources Used in This Article

- myFICO.com — FICO Score breakdown and factor weightings

- Consumer Financial Protection Bureau (CFPB) — cfpb.gov

- AnnualCreditReport.com — Official free credit report access

- Experian.com — Credit utilization guidance and score ranges

- Federal Trade Commission (FTC) — ftc.gov, credit repair and dispute rights

- National Consumer Law Center — nclc.org

Helpful Next Steps

If you’ve read this far, you’re already ahead of most people who just shrug at their score and move on. Here’s what I’d suggest doing this week, not someday:

- Pull your three free credit reports from AnnualCreditReport.com and actually read them.

- Download the Experian app to get your free FICO score.

- Write down your current balances and limits on every credit card and calculate your utilization ratio.

- Set up autopay on every account, even if it’s just the minimum.

- If you find an error, file a dispute this week while the motivation is fresh.

Credit isn’t a mystery. It’s a system with known rules, and once you understand those rules, you can play the game deliberately. Your score is not a verdict on your worth as a person — it’s a number that can be changed with the right information and enough consistent effort. good credit opens doors to wealth building

The door that slammed in my face years ago is now wide open. Yours can be too.

This article is intended for informational purposes only and does not constitute financial or legal advice. Always consult a certified financial planner or credit counselor for personalized guidance.

My name is Arshiyan Ahmed, and I write about personal finance because I’ve lived through the stress of financial uncertainty — and found my way out of it.

Over the past 7+ years, I’ve spent hundreds of hours studying budgeting systems, debt payoff strategies, and savings frameworks — not just in theory, but by applying them to real life. I’ve personally used the debt snowball method to eliminate credit card debt, built a 6-month emergency fund on a modest income, and helped friends and family create their first workable budgets.

I started Arshiyan Finance because I noticed one thing: most financial content online is either too complicated for beginners or too generic to be useful. I wanted to build a space where everyday people — whether you’re living paycheck to paycheck or just looking to manage money smarter — could find clear, actionable, and honest financial guidance without being sold something.

Everything I publish here is based on widely accepted financial principles, researched thoroughly, and written in plain language anyone can follow. The calculators, guides, and strategies on this site are the same tools I use and recommend to people I care about.

I’m not a licensed financial advisor, and nothing on this site is professional financial advice — but I do believe that access to good financial education can change lives. That’s why everything here is completely free.

When I’m not writing about money, I’m reading about it — because the more I learn, the better I can explain it to you.

Have a question or topic you’d like me to cover?