How to Plan for Retirement at Any Age

How to Plan for Retirement at Any Age

Table of Contents

- Retirement Planning Is Not Just for Old People

- What Retirement Actually Costs (The Number Nobody Wants to Face)

- The Retirement Accounts You Need to Understand

- Planning by Decade: Your 20s, 30s, 40s, 50s, and Beyond

- Step-by-Step: How to Build Your Personal Retirement Plan

- Mistakes That Set People Back Years

- Best Tools and Apps for Retirement Planning

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

My grandmother worked as a seamstress her entire adult life and retired at 68 with almost nothing saved. She got by on Social Security alone — $1,140 a month — for the last nineteen years of her life. She never complained, but I watched her quietly skip doctor visits she couldn’t afford, turn down family dinners because she couldn’t chip in, and decline vacations she’d talked about her whole life.

That image never left me. It became the reason I got obsessed with retirement planning — not the spreadsheet kind, but the real, human kind where you understand what’s at stake and what’s actually possible, no matter where you’re starting from.

Whether you’re 24 with your first paycheck or 55 with a growing sense of panic, this guide is the honest conversation about retirement that most people never have until it’s uncomfortably late. Read our financial guides

Trust note: The information in this article is drawn from IRS guidelines, Fidelity Investments research, the Employee Benefit Research Institute, and firsthand work with individuals navigating retirement planning at various life stages. This is educational content, not personalized financial advice. For decisions specific to your situation, a fee-only certified financial planner is your best resource.

Retirement Planning Is Not Just for Old People

Here’s a phrase you’ve probably heard: “Start saving early.” It’s good advice, but it’s repeated so often it has lost its teeth. People hear it, nod, and then go back to worrying about this month’s rent.

So let me try it a different way.

If you invest $200 a month starting at age 25 and earn an average annual return of 7%, you’ll have roughly $525,000 by age 65. If you wait until 35 to start the exact same habit, you end up with about $243,000. Same monthly investment. Same return. A ten-year delay costs you roughly $282,000.

That is not a small number. That is a paid-off house in a lot of American cities. That is the difference between choosing when you retire and being forced into it.

The point is not to shame anyone who started late — starting late is still infinitely better than not starting at all. The point is that time is the one ingredient in retirement planning that nobody can sell you more of once it’s gone.

What Retirement Actually Costs (The Number Nobody Wants to Face)

Most financial planners use a rule of thumb called the 4% rule — the idea that if you withdraw 4% of your portfolio each year in retirement, your money should last at least 30 years. Working backward from that rule, you can estimate your target retirement savings:

Take your expected annual retirement expenses and multiply by 25. That’s your ballpark number.

If you expect to spend $50,000 a year in retirement, you need $1.25 million saved.

If you expect to spend $70,000 a year, you’re looking at $1.75 million.

If you’re aiming for a simpler $40,000 lifestyle with Social Security covering part of that, your personal savings target shrinks considerably.

This feels overwhelming to many people until you remember that Social Security is meant to cover a portion of retirement income, and most people also carry paid-off assets like a home into retirement.

The AARP’s 2024 research suggests the average American household in retirement spends between $48,000 and $57,000 annually, depending on health status and geographic location. Healthcare is the line item that keeps growing — the Fidelity Retiree Health Care Cost Estimate for 2024 puts average medical spending for a retired couple at $330,000 over the course of retirement.

These numbers aren’t here to frighten you. They’re here so you can plan around reality rather than around hope.

start investing for retirement

The Retirement Accounts You Need to Understand

The U.S. government actually incentivizes retirement savings through tax-advantaged accounts. Using them correctly is one of the most reliable legal ways to keep more of your money.

401(k) or 403(b) — Employer Plans

If your employer offers a 401(k) with a matching contribution, funding it up to the match is as close to free money as the financial world gets. A typical match might be 50% of contributions up to 6% of your salary. If you earn $60,000 and contribute 6% ($3,600), your employer adds $1,800. That’s an immediate 50% return before the market does a thing.

For 2024, the contribution limit is $23,000 for those under 50, and $30,500 for those 50 and older (the extra $7,500 is called a catch-up contribution).

Traditional IRA

An Individual Retirement Account that you open yourself, independent of your employer. Contributions may be tax-deductible depending on your income and whether you have a workplace plan. Growth is tax-deferred, meaning you pay taxes when you withdraw in retirement. The 2024 contribution limit is $7,000, or $8,000 if you’re 50 or older.

Roth IRA

The Roth is contributed with after-tax dollars, but it grows completely tax-free. Withdrawals in retirement are also tax-free. For younger earners who expect to be in a higher tax bracket later in life, this is often the more valuable account in the long run. The same contribution limits apply as the Traditional IRA, but Roth eligibility phases out at higher income levels ($161,000 for single filers in 2024).

SEP-IRA and Solo 401(k)

For self-employed individuals and small business owners. The SEP-IRA allows contributions of up to 25% of net self-employment income, up to $69,000 in 2024. The Solo 401(k) has similar contribution capacity and is worth exploring if you have no employees.

The general funding priority most financial planners recommend: first, contribute to your 401(k) up to the employer match. Second, max out a Roth IRA if you’re eligible. Third, go back and max out the 401(k). After that, taxable brokerage accounts.

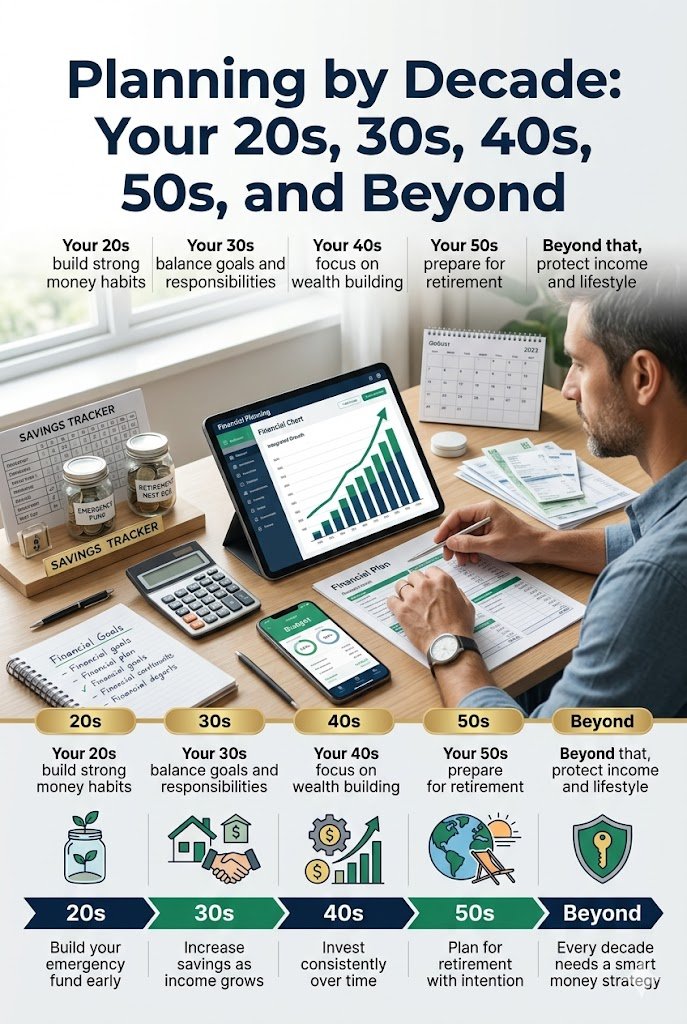

Planning by Decade: Your 20s, 30s, 40s, 50s, and Beyond

In Your 20s: Build the Habit, Not Just the Balance

The dollar amounts you save in your 20s matter less than forming the habit of saving consistently. Get enrolled in your employer’s 401(k) as early as possible. Open a Roth IRA — Fidelity and Vanguard both allow you to start one with no minimum balance. Aim to save 10 to 15% of your income even if that feels impossible right now. Start with 5% and increase it by 1% every time you get a raise.

Avoid lifestyle inflation. When your salary goes up, let your savings rate go up with it before your spending does.

emergency fund before retirement saving

In Your 30s: Optimize and Increase

Your 30s are often expensive. Mortgages, kids, bigger cars. The trap is watching retirement savings stagnate while everything else grows. The goal here is to hit the benchmarks: by age 35, aim to have saved roughly 1 to 2 times your annual salary.

If you have a growing income, prioritize closing the gap between what you’re saving and what you should be saving. Revisit your investment allocation — most people in their 30s should have significant equity exposure, since they have 30 or more years for the market to recover from downturns.

In Your 40s: Get Serious About the Gap

Your 40s tend to be peak earning years for many Americans. This is the decade to max out every tax-advantaged account you can. If you’re behind on savings, do not panic — but do take action. By age 45, a common benchmark is having 3 to 4 times your salary saved.

This is also the decade to start thinking seriously about what retirement actually looks like for you. Where will you live? What will you do? These aren’t idle daydreams — they directly shape your spending estimates, which shape your savings target.

In Your 50s: Catch-Up Mode

The IRS catch-up contribution provisions exist because they know many people arrive at their 50s behind schedule. Use them. Max your 401(k) at $30,500, max your IRA at $8,000.

Begin thinking about Social Security strategy. Claiming at 62 versus waiting until 70 can mean a difference of 76% in your monthly benefit. For most people who can afford to wait, delaying Social Security is one of the best financial decisions available.

In Your 60s: The Final Approach

Shift focus from accumulation to preservation. This does not mean abandoning growth entirely — a 65-year-old who retires may need their money to last 25 to 30 more years, so some equity exposure usually remains appropriate. But the volatility tolerance that served you in your 30s needs to be recalibrated.

Create a written retirement income plan that includes Social Security timing, Required Minimum Distributions from traditional accounts (which begin at age 73 under current law), and a withdrawal sequence strategy.

Step-by-Step: How to Build Your Personal Retirement Plan

Step 1: Know Where You Stand Right Now

Gather your current balances across every retirement account you own. Include old 401(k)s from previous jobs — an astounding $1.65 trillion in retirement savings sits forgotten in orphaned accounts according to Capitalize research. Track those down using the National Registry of Unclaimed Retirement Benefits at unclaimedretirementbenefits.com.

Step 2: Estimate Your Retirement Spending

Take your current monthly spending and adjust it for retirement. Some costs go down (commuting, work clothes, possibly a mortgage if it’s paid off). Others go up (healthcare, travel, hobbies). A rough starting estimate is 70 to 80% of your current income, though many active retirees spend as much as they did while working, especially in early retirement.

Step 3: Calculate Your Target Number

Use the 25x rule. Multiply your estimated annual retirement expenses by 25. That is your savings target from personal accounts, not counting Social Security.

Step 4: Get Your Social Security Estimate

Create an account at ssa.gov and review your earnings history and estimated benefit at different claiming ages. This is free and takes ten minutes. It is also consistently one of the most eye-opening things people do when they finally engage with retirement planning.

Step 5: Run the Numbers on Your Gap

Compare what you currently have (and its projected growth) to your target. The gap between those two numbers tells you exactly how much you need to save each month to close it. Tools like the Vanguard Retirement Income Calculator or Fidelity’s myPlan can run these projections for you.

Step 6: Automate Everything

The single most effective behavior change in retirement planning is removing the decision from your hands. Set up automatic contributions. Set up automatic increases. Let the system run so you don’t have to rely on willpower every payday.

Step 7: Revisit Once a Year

Your income changes. Your life changes. Your spending projections change. A one-hour annual review of your retirement plan keeps things calibrated without turning into a second job.

Mistakes That Set People Back Years

Cashing out a 401(k) when changing jobs. It feels like found money, but between income taxes and a 10% early withdrawal penalty, you lose 30 to 40 cents on every dollar. Always roll it into an IRA or your new employer’s plan.

Saving without investing. Money sitting in a savings account earning 0.5% annually is essentially losing ground to inflation every year. Retirement contributions need to be invested — in index funds, target-date funds, or something else — not just deposited and forgotten.

Ignoring the employer match. Leaving employer matching contributions unclaimed is genuinely one of the most expensive financial mistakes a person can make. It is a guaranteed 50 to 100% return on your contribution that disappears if you don’t take it.

Planning to work forever as a retirement strategy. Health changes, layoffs, caregiving responsibilities, and industry shifts force many people out of the workforce earlier than they intended. Relying on “I’ll just keep working” as a plan is risky. The data backs this up: roughly half of retirees leave the workforce earlier than planned, according to the Employee Benefit Research Institute.

Carrying high-interest debt into retirement. Interest rates on credit cards often run between 20 and 27%. No realistic investment return consistently beats that. Eliminating high-interest debt before and during the accumulation phase is as important as growing your savings.

tax-advantaged retirement accounts

Treating retirement accounts as emergency funds. Every early withdrawal comes with taxes, penalties, and the loss of future compounding growth. A separate emergency fund with three to six months of expenses protects your retirement savings from life’s unpredictability.

Best Tools and Apps for Retirement Planning

Fidelity myPlan — Built into the Fidelity platform, this tool projects your retirement income, shows your gap, and lets you test different contribution scenarios. It pulls data directly from your Fidelity accounts, which makes it more accurate than standalone calculators.

https://www.planviewer.fidelity.co.uk/newlogin

Vanguard Retirement Income Calculator — Clean, simple, and credible. Vanguard’s conservative assumptions mean the projections tend to be on the cautious side, which is arguably a feature rather than a bug for long-term planning.

https://investor.vanguard.com/tools-calculators/retirement-income-calculator

Personal Capital (now Empower) — A free financial dashboard that aggregates all your accounts in one place. Its retirement planner feature runs Monte Carlo simulations to show you the probability of your savings lasting through retirement. Genuinely impressive for a free tool.

https://www.empower.com/empower-personal-wealth-transition

Mint or YNAB (You Need a Budget) — Understanding your current spending is foundational to estimating retirement spending. Both apps track transactions and categorize expenses. YNAB has a steeper learning curve but is more powerful for intentional budgeters.

SSA.gov My Social Security Portal — Free, official, and essential. Your estimated benefit statement lives here and should be reviewed every year or two to catch errors in your earnings record before they become permanent.

Betterment or Wealthfront — Robo-advisors that automatically invest your IRA contributions in a diversified, low-cost portfolio adjusted for your retirement timeline. Both charge roughly 0.25% per year in management fees, which is extremely low compared to traditional advisory fees.

https://invest.wealthfront.com/wealthfront-vs-betterment

Frequently Asked Questions

What if I am 45 with almost nothing saved? Is it too late?

No. It is genuinely not too late. A person who starts saving aggressively at 45 and works until 67 has 22 years of contributions and growth ahead of them. Combined with Social Security and catch-up contribution limits after 50, meaningful retirement security is still achievable. It requires discipline, but it is within reach.

Should I pay off debt or save for retirement first?

It depends on the interest rate. High-interest debt, anything above 7 or 8%, should generally be aggressively paid down before maximizing retirement savings. The exception is always to capture the full employer match first — that return beats even high-interest debt. Low-interest debt like a mortgage can often be carried alongside healthy retirement contributions.

How does Social Security factor into my retirement plan?

For most Americans, Social Security replaces roughly 40% of pre-retirement income, though it is lower as a percentage for higher earners. It should be treated as a foundation, not a full plan. The key decision is when to claim it — every year you delay past 62 (up to age 70) increases your benefit by roughly 6 to 8%.

What is a target-date fund and should I use one?

A target-date fund is a single mutual fund that automatically shifts from aggressive growth investments to more conservative ones as you approach your target retirement year. A 2045 fund, for example, holds mostly stocks now and gradually moves toward bonds as 2045 approaches. They are a perfectly reasonable choice for people who want a hands-off, low-maintenance investment approach.

Can I have both a 401(k) and an IRA at the same time?

Yes, absolutely. They are separate account types and you can contribute to both in the same year, subject to the respective limits. Having both allows you to save more and potentially use both tax-deferred and tax-free growth strategies simultaneously.

Sources Used in This Article

- Fidelity Investments — 2024 Retiree Health Care Cost Estimate and retirement benchmark guidelines

- Employee Benefit Research Institute — ebri.org (retirement confidence surveys and early retirement statistics)

- Social Security Administration — ssa.gov (benefit calculators and claiming strategies)

- IRS.gov — Retirement plan contribution limits and catch-up provisions for 2024

- AARP — aarp.org (average retirement spending research)

- Capitalize Research — missingretirementaccounts.com (orphaned 401k data)

- Vanguard — vanguard.com (investment return assumptions and retirement income research)

Helpful Next Steps

Retirement planning has a funny quality to it. It feels distant and abstract for most of your life, and then suddenly it feels urgent and overwhelming. The window where it feels just right — important but manageable — is always right now, regardless of your age.

Here are five things worth doing this week:

- Log into ssa.gov and check your Social Security earnings record and estimated benefit. It takes ten minutes and surprises almost everyone.

- Find every retirement account you currently own, including any from past employers. Consolidate dormant accounts into an IRA you actively manage.

- Check whether you’re capturing your full employer 401(k) match. If you aren’t, change your contribution rate before your next paycheck.

- Run your numbers through the Empower retirement planner or Fidelity myPlan to see where you actually stand relative to your target.

- Set one automatic increase — either starting a new contribution or bumping an existing one by even 1% of your income.

My grandmother never got to take the trips she talked about. She never saw the Pacific Ocean. For years I was sad about that, and then I decided to turn it into something useful. This guide is part of that.

Retirement planning is not about being rich. It is about having choices when you’re older. And the choices available to you are largely determined by the decisions you make today.

Start now. Adjust later. The important thing is to begin.

Try our free calculators: compound interest calculator

Try our free calculators: savings goal calculator

This article is intended for general educational purposes only and does not constitute personalized financial, investment, or legal advice. Consult a licensed financial professional before making retirement planning decisions specific to your circumstances.

My name is Arshiyan Ahmed, and I write about personal finance because I’ve lived through the stress of financial uncertainty — and found my way out of it.

Over the past 7+ years, I’ve spent hundreds of hours studying budgeting systems, debt payoff strategies, and savings frameworks — not just in theory, but by applying them to real life. I’ve personally used the debt snowball method to eliminate credit card debt, built a 6-month emergency fund on a modest income, and helped friends and family create their first workable budgets.

I started Arshiyan Finance because I noticed one thing: most financial content online is either too complicated for beginners or too generic to be useful. I wanted to build a space where everyday people — whether you’re living paycheck to paycheck or just looking to manage money smarter — could find clear, actionable, and honest financial guidance without being sold something.

Everything I publish here is based on widely accepted financial principles, researched thoroughly, and written in plain language anyone can follow. The calculators, guides, and strategies on this site are the same tools I use and recommend to people I care about.

I’m not a licensed financial advisor, and nothing on this site is professional financial advice — but I do believe that access to good financial education can change lives. That’s why everything here is completely free.

When I’m not writing about money, I’m reading about it — because the more I learn, the better I can explain it to you.

Have a question or topic you’d like me to cover?