Understanding Taxes: What Every Earner Should Know

Understanding Taxes: What Every Earner Should Know

Table of Contents

- Why Taxes Feel So Confusing (And Why They Don’t Have to Be)

- The Different Types of Taxes Americans Pay

- How the Federal Income Tax Bracket System Actually Works

- The Difference Between a Tax Deduction and a Tax Credit

- Step-by-Step: How to Prepare and File Your Taxes

- Mistakes That Cost People Real Money Every Year

- Best Tools and Apps for Tax Season

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

The first time I ever filed my own taxes, I sat at my kitchen table for two hours staring at a Form W-2 like it was written in ancient Sumerian. My dad had always handled it. My college didn’t teach it. And the IRS website, bless its heart, reads like a legal document translated by a committee that had never met a regular person.

I ended up overpaying by nearly $800 that year because I simply didn’t know about deductions I qualified for. That mistake stuck with me. Since then, I’ve spent years breaking down the U.S. tax system into plain language — not to give legal advice, but to make sure nobody else sits at that kitchen table feeling as lost as I did. Read our financial guides

This article is that conversation I wish I’d had earlier.

Trust note: Everything in this article is based on current IRS guidelines, verified tax education resources, and firsthand experience helping everyday earners understand their obligations. This is not tax or legal advice. For your specific situation, always consult a licensed CPA or enrolled agent.

Why Taxes Feel So Confusing (And Why They Don’t Have to Be)

Part of the problem is that Americans deal with multiple layers of taxation simultaneously — federal, state, and sometimes local. On top of that, the rules change slightly every year. New brackets, new limits, adjusted standard deductions. It’s like trying to follow a recipe where someone moves the goalposts between batches.

But here’s the thing: for most ordinary earners — salaried employees, part-time workers, freelancers, and small business owners — the core concepts haven’t changed all that much. Once you understand the foundation, the updates are just small adjustments to a structure you already know. taxes on your side income

The goal of this guide is to hand you that foundation.

The Different Types of Taxes Americans Pay

Before getting into income taxes specifically, it helps to zoom out and see the full picture of where your money goes.

Federal Income Tax is what most people think of when they hear the word “taxes.” It’s paid to the IRS, calculated on your total income after deductions, and follows a progressive bracket system (more on that shortly).

State Income Tax varies dramatically depending on where you live. States like Texas, Florida, and Nevada have no state income tax at all. Others, like California and New York, have some of the highest rates in the country. If you live in a high-tax state, this can add a meaningful chunk to your total tax bill.

FICA Taxes are the ones that quietly leave your paycheck before you even see it. FICA stands for Federal Insurance Contributions Act, and it covers Social Security (6.2% of your wages) and Medicare (1.45%). Your employer matches those amounts. Self-employed people pay both sides, which adds up to 15.3% — a number that surprises a lot of new freelancers.

Sales Tax is what you pay at the register. It’s a state-level tax, and rates vary from zero in some states to over 10% in parts of Louisiana and Tennessee when local taxes are added in.

Property Tax is paid by homeowners and is determined by your local government based on the assessed value of your property. It funds things like public schools, roads, and local services.

Understanding that you’re juggling several different tax obligations at once — not just the federal one — gives you a much more honest picture of your true tax burden.

How the Federal Income Tax Bracket System Actually Works

This is the concept that trips up more people than almost anything else. A common belief goes something like this: “If I get a raise and move into a higher tax bracket, I’ll take home less money.” That is not how it works — not even close.

The U.S. uses a marginal tax system. This means only the portion of your income that falls within a given bracket gets taxed at that bracket’s rate. Think of it like filling buckets. The first bucket holds income up to a certain threshold and gets taxed at the lowest rate. Once that bucket is full, income starts filling the next one at a slightly higher rate. And so on.

For 2024, the federal income tax brackets for a single filer look like this:

| Tax Rate | Income Range |

|---|---|

| 10% | Up to $11,600 |

| 12% | $11,601 to $47,150 |

| 22% | $47,151 to $100,525 |

| 24% | $100,526 to $191,950 |

| 32% | $191,951 to $243,725 |

| 35% | $243,726 to $609,350 |

| 37% | Over $609,350 |

So if you earn $55,000, you are NOT paying 22% on all of it. You pay 10% on the first $11,600, then 12% on the next chunk, and 22% only on the portion above $47,150. Your effective tax rate — the actual percentage of your total income that goes to taxes — ends up being much lower than your marginal bracket suggests.

A quick example: A single filer earning $55,000 has an effective federal tax rate closer to 13% after the standard deduction is applied. Not 22%.

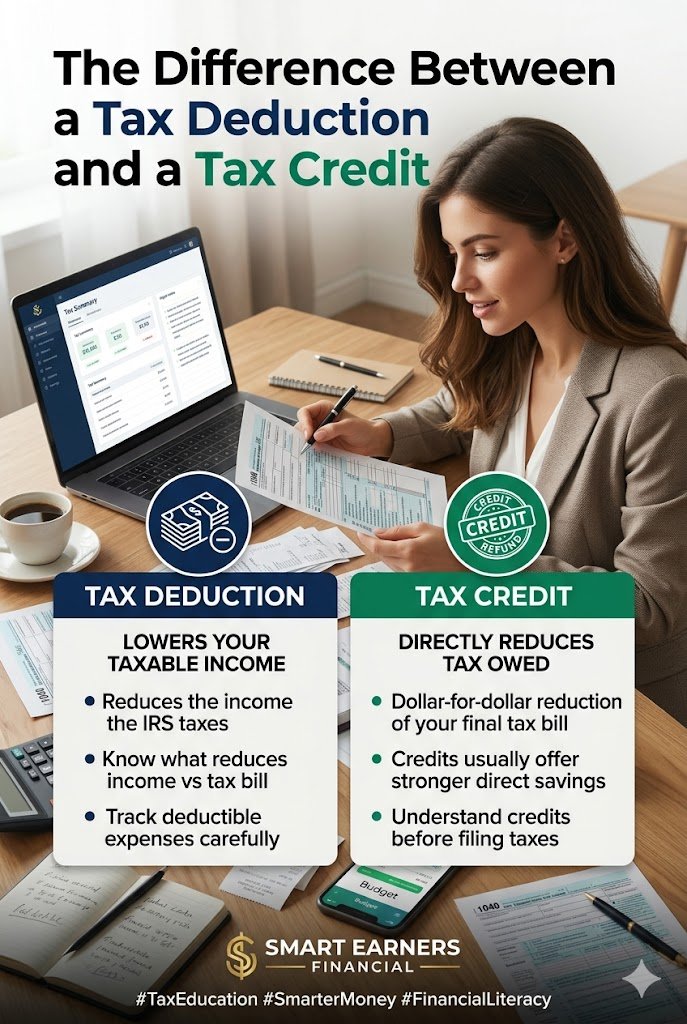

The Difference Between a Tax Deduction and a Tax Credit

These two terms often get used interchangeably, but they work very differently — and confusing them costs people money. tax-efficient investing strategies

A tax deduction reduces your taxable income. If you earn $60,000 and claim $10,000 in deductions, the IRS taxes you as if you earned $50,000. The actual value of a deduction depends on your bracket. A $1,000 deduction saves a person in the 22% bracket $220. The same deduction saves someone in the 12% bracket only $120.

A tax credit reduces your actual tax bill dollar for dollar. A $1,000 tax credit means you owe $1,000 less in taxes, period — regardless of your bracket. Credits are generally more powerful than deductions of the same amount.

Some credits are also refundable, which means if the credit wipes out your entire tax bill and there’s still credit left over, the IRS sends you the difference as a refund. The Earned Income Tax Credit (EITC) and the Child Tax Credit work this way and put real money back in the pockets of lower and middle-income earners every year.

Common deductions to know:

- Standard deduction (for 2024: $14,600 for single filers, $29,200 for married filing jointly)

- Mortgage interest deduction

- Student loan interest (up to $2,500)

- Contributions to a traditional IRA or 401(k)

- Self-employment business expenses

Common credits to know:

- Earned Income Tax Credit

- Child Tax Credit (up to $2,000 per qualifying child)

- American Opportunity Tax Credit (for college expenses)

- Child and Dependent Care Credit

Step-by-Step: How to Prepare and File Your Taxes

Step 1: Gather Your Documents

Before touching any software, collect everything. You’ll need:

- W-2 forms from all employers (mailed or available through your employer’s HR portal)

- 1099 forms if you did freelance work, earned interest, or had investment income

- Records of any deductible expenses

- Last year’s tax return (for reference)

- Your Social Security number and the same for any dependents

Step 2: Choose Your Filing Status

Your status affects your bracket thresholds and standard deduction. Common statuses include Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse. Head of Household, for example, offers a higher standard deduction than Single and is available to unmarried people who support a dependent.

Step 3: Decide Whether to Take the Standard Deduction or Itemize

For most Americans, the standard deduction is larger than the sum of their itemized deductions — especially since the Tax Cuts and Jobs Act of 2017 nearly doubled it. But if you own a home with a large mortgage, made significant charitable contributions, or have heavy medical expenses, itemizing may save you more. Run both numbers before deciding.

Step 4: Use Reliable Tax Software or a Professional

For straightforward W-2 returns, free filing options are excellent. For more complex situations — self-employment, rental income, stock sales — either use a more robust software or hire a CPA.

Step 5: Double-Check for Credits You Might Be Missing

Before submitting, review whether you qualify for the EITC, Child Tax Credit, education credits, or energy-efficiency credits for home improvements. These are frequently overlooked.

Step 6: File Electronically and Set Up Direct Deposit

E-filing is faster, more secure, and reduces errors. Adding direct deposit for your refund typically gets money in your account within 10 to 21 days.

Step 7: Keep Records for at Least Three Years

The IRS has three years from your filing date to audit a return under normal circumstances. Store your returns and supporting documents — physical or digital — for at least that long. For self-employment income, keep records for six years.

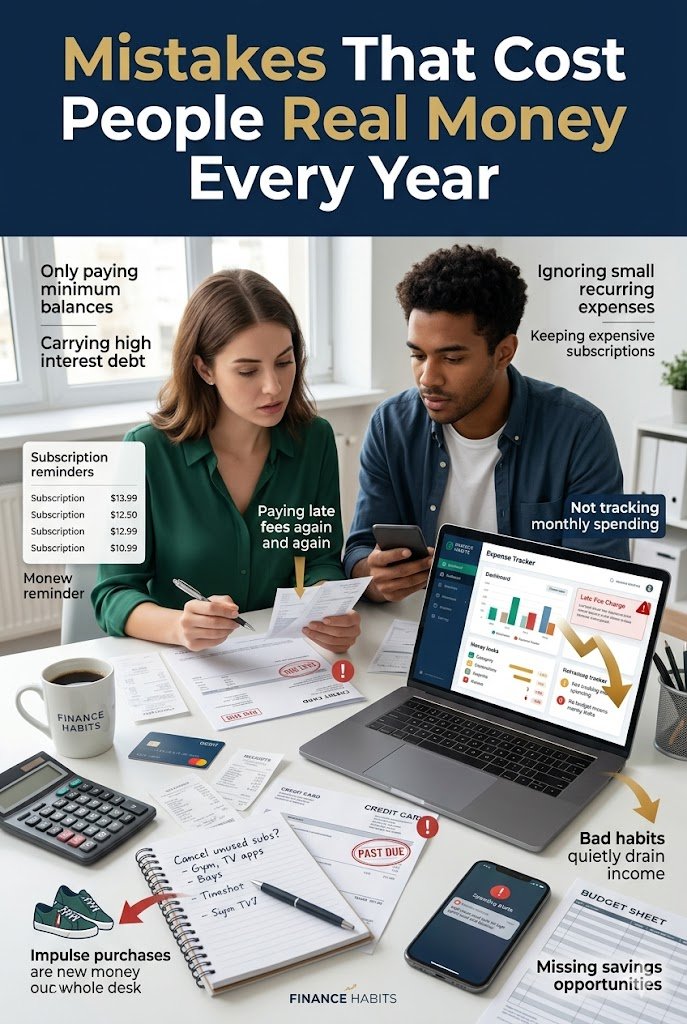

Mistakes That Cost People Real Money Every Year

Not filing at all because you think you don’t owe anything. Even if your income is low and you owe no taxes, you may still qualify for refundable credits like the EITC. Not filing means leaving that money on the table. The IRS won’t chase you down to hand it to you.

Missing the self-employment tax reality. New freelancers are often blindsided by the 15.3% self-employment tax on top of income tax. Setting aside 25 to 30% of every payment received is a safe habit while you’re still figuring out your numbers.

Forgetting to report side income. Income from platforms like Etsy, Uber, Airbnb, or even PayPal transfers over $600 should be reported. The IRS receives 1099-K forms from these platforms and cross-references them against your return.

Claiming a deduction without documentation. You can absolutely deduct legitimate business expenses — but if the IRS ever asks, you need receipts, invoices, or bank statements to prove it. “I remember buying it” is not sufficient.

Filing with the wrong status. Choosing Single instead of Head of Household when you qualify for the latter costs you a meaningful amount in deductions. The difference in standard deduction between the two is over $5,000 for 2024.

Waiting until April 14th to start. Filing under pressure leads to careless mistakes. Errors slow your refund, and in worst cases, they trigger correspondence from the IRS that takes months to resolve.

Best Tools and Apps for Tax Season

TurboTax remains the most widely used consumer tax software. It holds your hand through every question, catches common errors, and offers live CPA access if you hit something complicated. The free version covers simple W-2 returns; the self-employed edition handles freelance income well.

H&R Block Online is a strong competitor to TurboTax, often at a lower price point. Their interface is clean and their free tier covers more situations than TurboTax’s. They also have physical locations if you prefer to sit down with someone in person.

FreeTaxUSA is an underrated option for people who are comfortable doing their own taxes and want to avoid the premium price tags. Federal filing is free for everyone; state returns cost a small fee.

IRS Free File at irs.gov is the official government program that allows eligible taxpayers (generally those earning under $79,000) to file for free through partner software companies. No upsells, no credit card required.

https://apps.irs.gov/app/freefile

MileIQ is an app that runs quietly in the background and automatically logs mileage using your phone’s GPS. For anyone who drives for work purposes, it pays for itself many times over in documented deductions.

QuickBooks Self-Employed is worth considering for freelancers who want year-round tracking of income and expenses rather than a last-minute scramble every April. It categorizes transactions, tracks mileage, and estimates quarterly taxes automatically.

https://quickbooks.intuit.com/solopreneur

Frequently Asked Questions

What happens if I miss the April 15th deadline?

You can request an automatic six-month extension using IRS Form 4868. This gives you until October 15th to file. Critically, the extension is for filing only — not for paying. If you owe taxes, interest and penalties start accruing from the original deadline. Estimate what you owe and pay it by April 15th even if you need more time to finalize your return.

Do I have to pay taxes on a gift I received?

Generally no. Gift taxes are paid by the giver, not the recipient, and even then most gifts fall well under the annual exclusion limit ($18,000 per person per year in 2024). Inheritances are also typically not counted as taxable income to the recipient, though estate taxes may apply at the estate level for very large amounts.

I worked two jobs last year. Will I owe more taxes?

Possibly. When you work multiple jobs, each employer withholds taxes as if that job is your only income. Combined, your total income may push you into a higher bracket than either employer accounted for. Review your withholding using the IRS Tax Withholding Estimator tool to see if you should adjust your W-4.

Should I hire a CPA or file on my own?

If your situation is simple — a W-2 job, no investments, no business income — quality software is genuinely sufficient. If you’re self-employed, have rental properties, experienced a major life event like a divorce or inheritance, or simply want peace of mind, a CPA or enrolled agent earns their fee many times over.

What is a quarterly estimated tax and do I need to pay it?

If you expect to owe $1,000 or more in federal taxes and don’t have an employer withholding taxes for you, the IRS expects you to pay in four installments throughout the year — in April, June, September, and January. Missing these payments results in an underpayment penalty, even if you pay the full amount when you file in April.

Sources Used in This Article

- Internal Revenue Service — irs.gov (tax brackets, forms, deductions, credits)

- IRS Publication 17 — Your Federal Income Tax (For Individuals)

- IRS Publication 334 — Tax Guide for Small Business

- Tax Foundation — taxfoundation.org (state tax comparisons, effective rate data)

- Consumer Financial Protection Bureau — cfpb.gov

- National Society of Accountants — nsacct.org (average tax preparation fees)

Helpful Next Steps

Taxes reward the prepared and quietly punish the disorganized. The good news is that being prepared doesn’t require a finance degree — it just requires building a few simple habits and knowing where to look. Try free tool savings goal calculator

Here’s what to do before your next filing season:

- Create a simple folder — physical or digital — where you drop every tax-related document as it arrives.

- If you’re self-employed, start tracking income and deductible expenses monthly rather than annually. QuickBooks Self-Employed or even a basic spreadsheet works.

- Use the IRS Withholding Estimator at irs.gov to check whether you’re on track with your withholding and avoid a surprise bill in April.

- Bookmark IRS Free File or choose your preferred software early so you’re not making rushed decisions in mid-April.

- If your situation changed significantly this year — new job, new baby, new home, new side business — consider a one-time consultation with a CPA just to make sure you’re set up correctly going forward.

Taxes are one of those things that feel overwhelming until the moment they don’t. That shift usually happens the first time you actually understand what you’re looking at — and realize the system, while imperfect, is far less mysterious than it seemed from the outside.

You don’t need to love taxes. You just need to stop being afraid of them.

This article is intended for general educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change regularly. Consult a qualified tax professional for advice specific to your situation.

My name is Arshiyan Ahmed, and I write about personal finance because I’ve lived through the stress of financial uncertainty — and found my way out of it.

Over the past 7+ years, I’ve spent hundreds of hours studying budgeting systems, debt payoff strategies, and savings frameworks — not just in theory, but by applying them to real life. I’ve personally used the debt snowball method to eliminate credit card debt, built a 6-month emergency fund on a modest income, and helped friends and family create their first workable budgets.

I started Arshiyan Finance because I noticed one thing: most financial content online is either too complicated for beginners or too generic to be useful. I wanted to build a space where everyday people — whether you’re living paycheck to paycheck or just looking to manage money smarter — could find clear, actionable, and honest financial guidance without being sold something.

Everything I publish here is based on widely accepted financial principles, researched thoroughly, and written in plain language anyone can follow. The calculators, guides, and strategies on this site are the same tools I use and recommend to people I care about.

I’m not a licensed financial advisor, and nothing on this site is professional financial advice — but I do believe that access to good financial education can change lives. That’s why everything here is completely free.

When I’m not writing about money, I’m reading about it — because the more I learn, the better I can explain it to you.

Have a question or topic you’d like me to cover?